Introduction

Raising your first fund is hard. You are not just pitching your strategy, your access, and your track record – you are also pitching yourself. And while the opportunity you are pursuing may be clear in your own mind, it’s something else entirely to translate that into a narrative LPs believe in (and are willing to back).

At Sydecar, we’ve spoken to dozens of emerging fund managers about their biggest challenges. Repeatedly, the same themes surfaced. Fund managers are focused on crafting a story that resonates, building credibility without a long track record, tailoring materials for different LP personas, and figuring out how to convey legitimacy.

This checklist is designed to help you navigate the fundraising process. It will help you ask the right questions, avoid common pitfalls, and build a foundation that makes your fundraising smoother, faster, and more effective.

Let’s get into it.

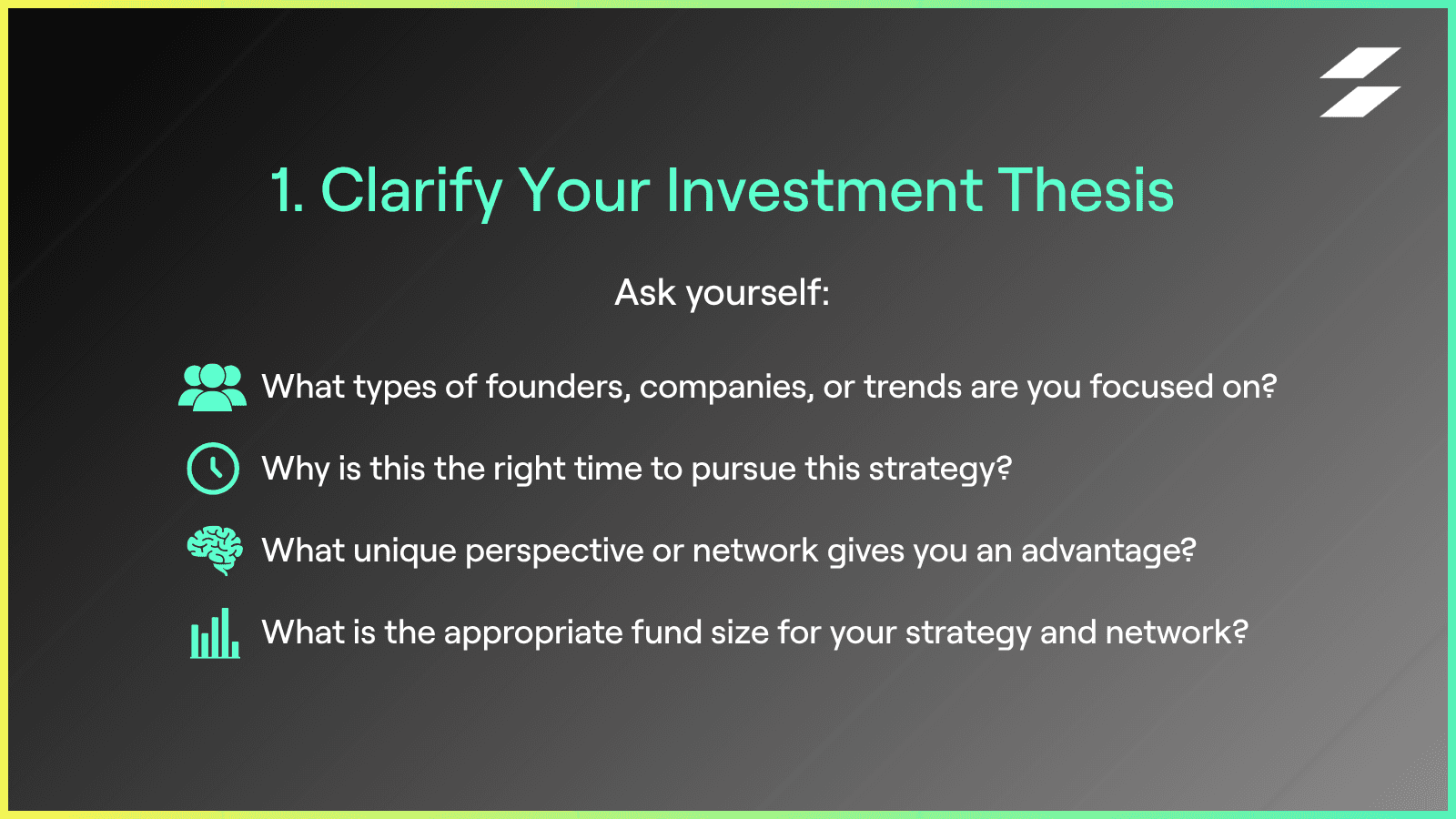

1. Clarify Your Investment Thesis

Your thesis goes beyond a slide in your deck. It is your compass. A strong thesis clearly communicates what you invest in, why you’re doing it, and how you will win.

Too many managers default to vague language or overly broad strategies. LPs want to understand your focus, your edge, and your conviction.

Ask yourself:

What types of founders, companies, or trends are you focused on?

Why is this the right time to pursue this strategy?

What unique perspective or network gives you an advantage?

What is the appropriate fund size for your strategy and network?

A common pitfall among emerging managers is assuming they’ll raise a $20M fund, only to scale that target down to $3–5M once fundraising begins. Clarifying your fund size from the outset leads to a more achievable raise, a stronger narrative, and a clearer vision for your fund.

A good thesis is specific, directional, and rooted in your experience. It should be clear enough that someone else could repeat it back to you after a single meeting.

Example fund thesis:

“Quantum Capital is launching a $5 M pre‑seed fund in Boston to back MIT and Harvard quantum computing spinouts. We leverage the GP’s quantum physics PhD and experience commercializing three university patents. With recent advances in quantum hardware and increased federal funding, now is the time to bridge academic research and commercial application.”

This example demonstrates:

Stage and fund size: $5 M pre‑seed

Geographic & sector focus: Quantum computing spinouts at MIT/Harvard

Differentiation: PhD and proven experience in commercializing university patents

Why now: Technological and funding tailwinds

This level of clarity helps LPs instantly grasp what the fund is doing, why the manager is qualified, and how value will be created, making the thesis compelling and memorable.

2. Build Your Narrative

LPs are evaluating your fund strategy as much as they are evaluating you. That means your personal and professional stories need to connect directly to your investment thesis. Maybe you have spent a decade operating in the space you now invest in. Maybe you have built a community that gives you proprietary access to deals. Whatever the case, your background should reinforce your credibility and signal that you know how to pick winners within your thesis.

For many emerging managers, especially those without a traditional background, crafting a personal narrative that reinforces their investment thesis is one of the most important parts of fundraising. Whether they say it or not, many LPs carry a mental image of who a “fundable GP” is. If you do not match that image, you will need to work even harder to build trust.

At first, this may seem like a disadvantage. In reality, it is an opportunity to differentiate and highlight the unique value your background brings.

A compelling narrative can help LPs understand what makes you uniquely qualified to execute your thesis. It can spotlight the experiences, networks, and insights that conventional backgrounds might not offer.

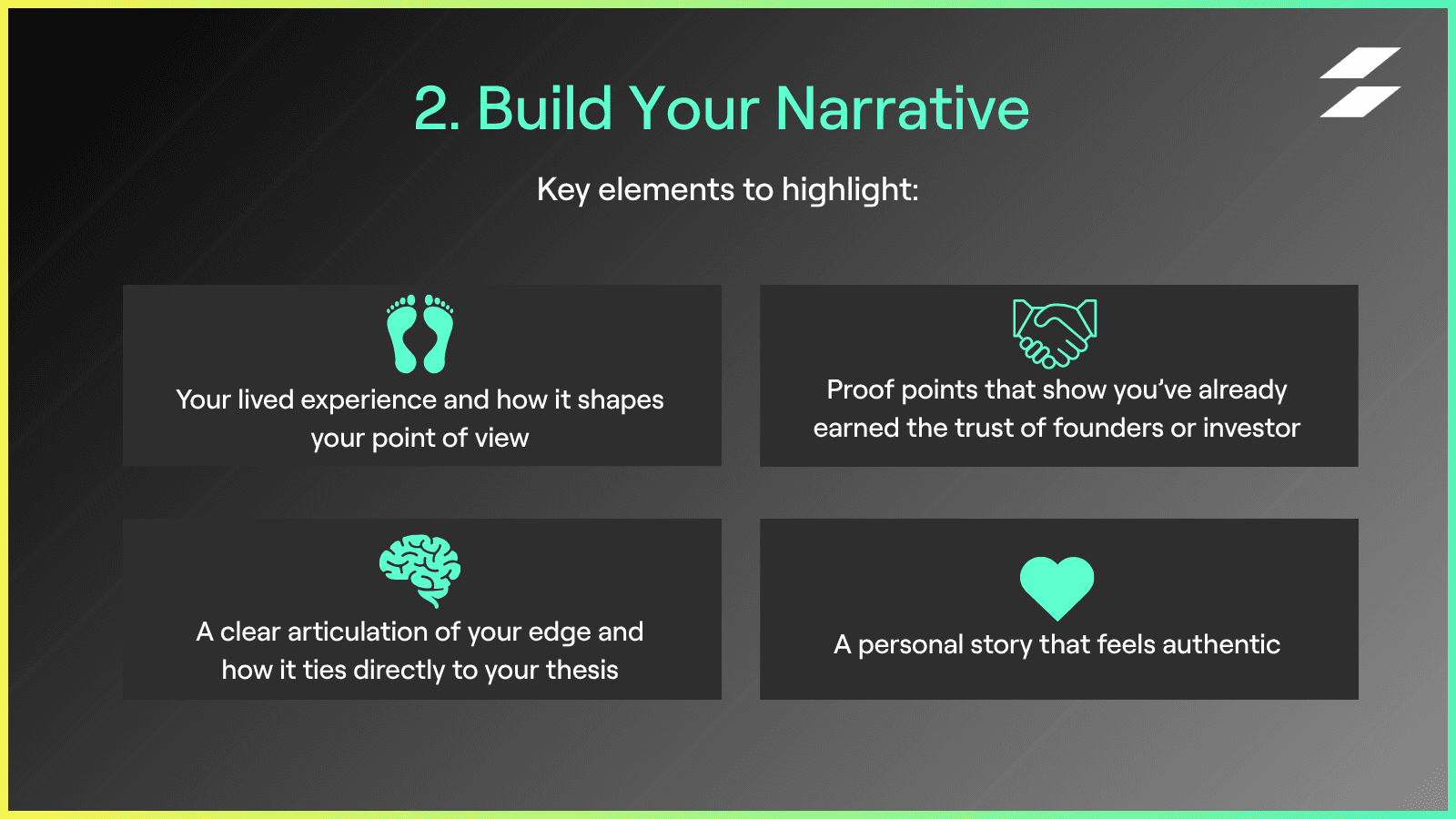

Key elements to highlight:

Your lived experience and how it shapes your point of view

Proof points that show you’ve already earned the trust of founders or investors

A clear articulation of your edge and how it ties directly to your thesis

A personal story that feels authentic

Remember, your goal is not to mimic someone else’s success story. It is to make a clear and credible case for your own. Colin Gardiner, GP of Yonder Ventures, is a great example of how a personal track record can reinforce a fund’s investment thesis.

Colin spent 15 years building marketplaces that raised hundreds of millions of dollars and generated billions in GMV. Through that experience, he developed a deep conviction in his ability to identify high-potential marketplace startups. That conviction, and his desire for greater financial upside in the companies he was already advising, ultimately led him to launch his first fund. Read more about how Colin went from operator to building a 200+ investor syndicate in 6 months here.

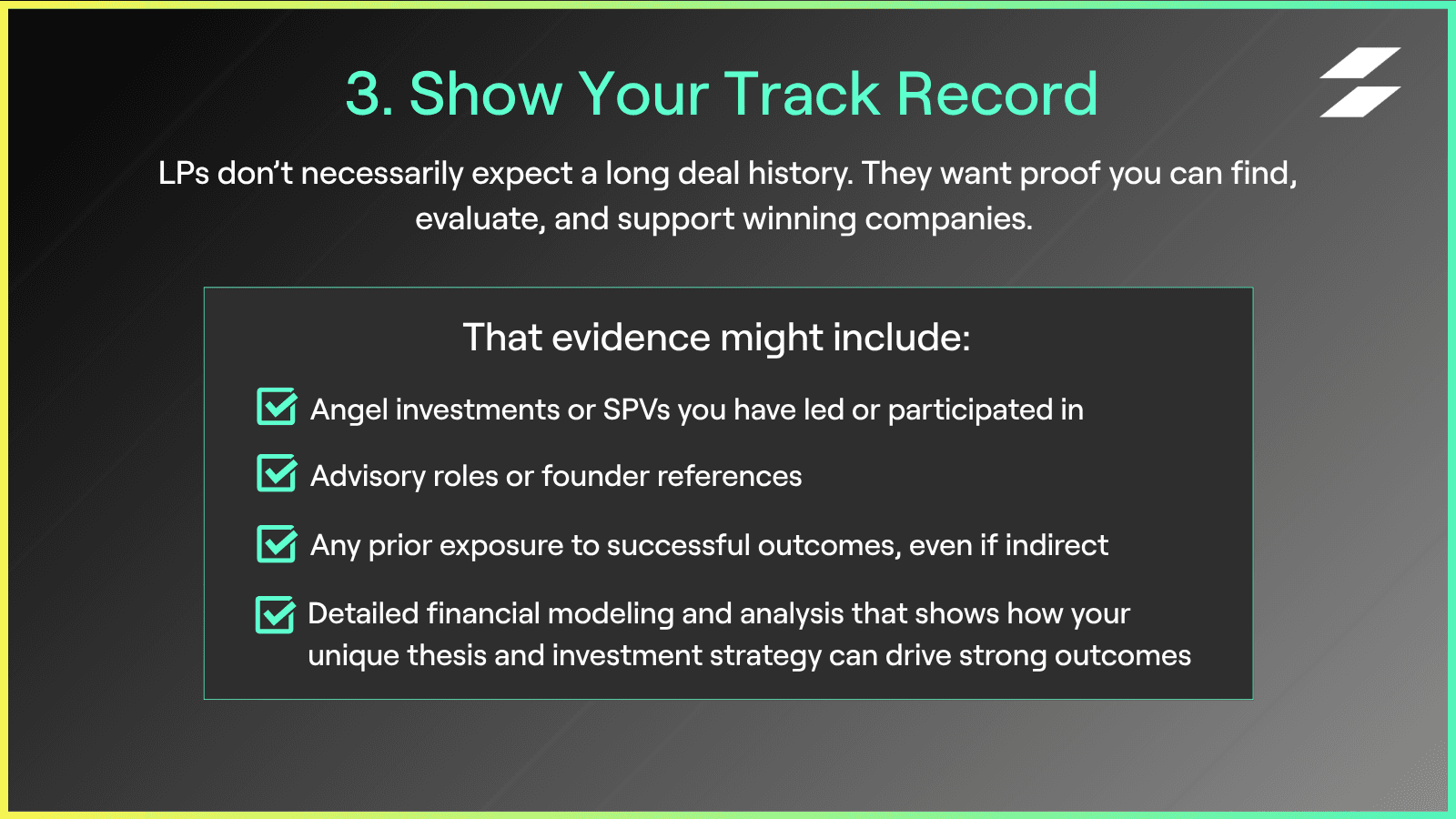

3. Show Your Track Record

Emerging managers often worry they do not have a “real” track record. But LPs who are accustomed to backing emerging managers don’t necessarily expect you to have led multiple deals. They are looking for evidence that you can find, evaluate, and support winning companies.

That evidence might include:

Angel investments or SPVs you have led or participated in

Advisory roles or founder references

Any prior exposure to successful outcomes, even if indirect

Detailed financial modeling and analysis that shows how your unique thesis and investment strategy can drive strong outcomes

Rather than proving that you have already succeeded as a fund manager, your goal should be to show that you have the judgment, relationships, and access needed to succeed in the future.

And if you don’t have a formal track record? Think about how to show momentum, such as founder references, diligence processes, or syndicates you have built. You can also lean into your access: many successful emerging managers win LP trust by surfacing investment opportunities that would otherwise be out of reach for traditional investors. Demonstrating that you have visibility into high-potential, under-the-radar deals can be just as compelling as a formal track record.

For example, maybe you’ve built deep ties within the Latin American fintech ecosystem and can identify promising companies early, making introductions or facilitating connections to oversubscribed rounds that institutional investors might not otherwise know about. Your network alone could demonstrate a differentiated edge and help build LP confidence in your ability to access unique opportunities.

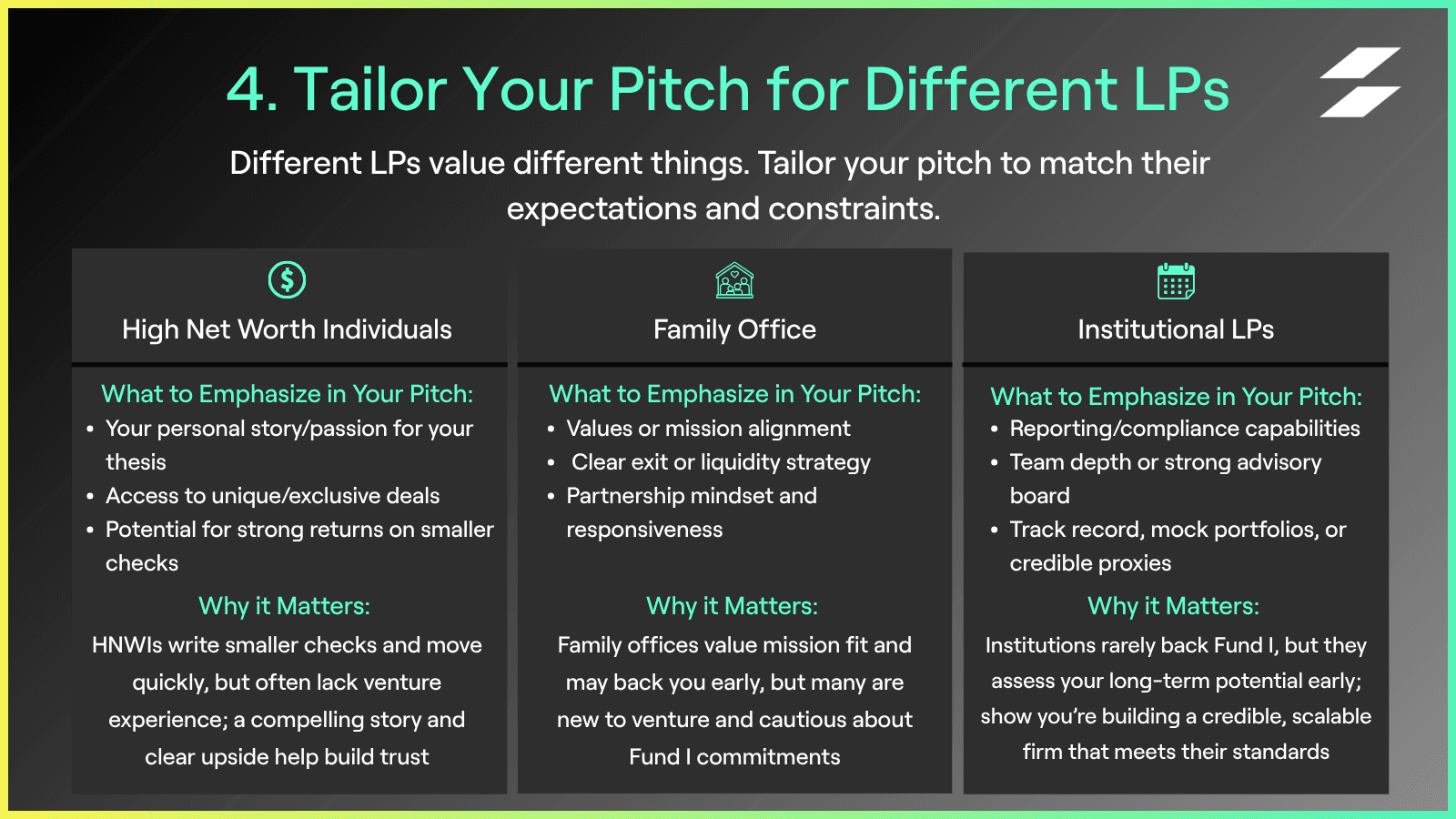

4. Tailor Your Pitch for Different LPs

Different LPs prioritize different criteria. Family offices, high-net-worth individuals, registered investment advisors, and institutions each have very different expectations around reporting, minimums, communication style, and diligence.

That is why “one-size-fits-all” decks usually fall flat.

Before each meeting, answer questions like:

What type of LP am I speaking to?

What is their typical check size and investment horizon?

Are they looking for frequent updates, hands-off reporting, or hands-on partnership?

Tailoring your pitch does not mean rewriting your entire story, but it does mean knowing what to emphasize, what questions to anticipate, and what materials to prepare.

It also means knowing your audience and focusing your time on those most likely to commit. While family offices and institutional investors often express interest in building relationships with emerging managers, they may wait until Fund II or Fund III to write checks. Many first-time managers spend months in conversations with these groups, only to realize they were never seriously considering a Fund I investment. Being realistic about who’s most likely to convert helps you avoid wasted cycles and stay focused on LPs who are actively allocating to first-time funds.

Use the guide below to align your pitch with what matters most to each type of LP:

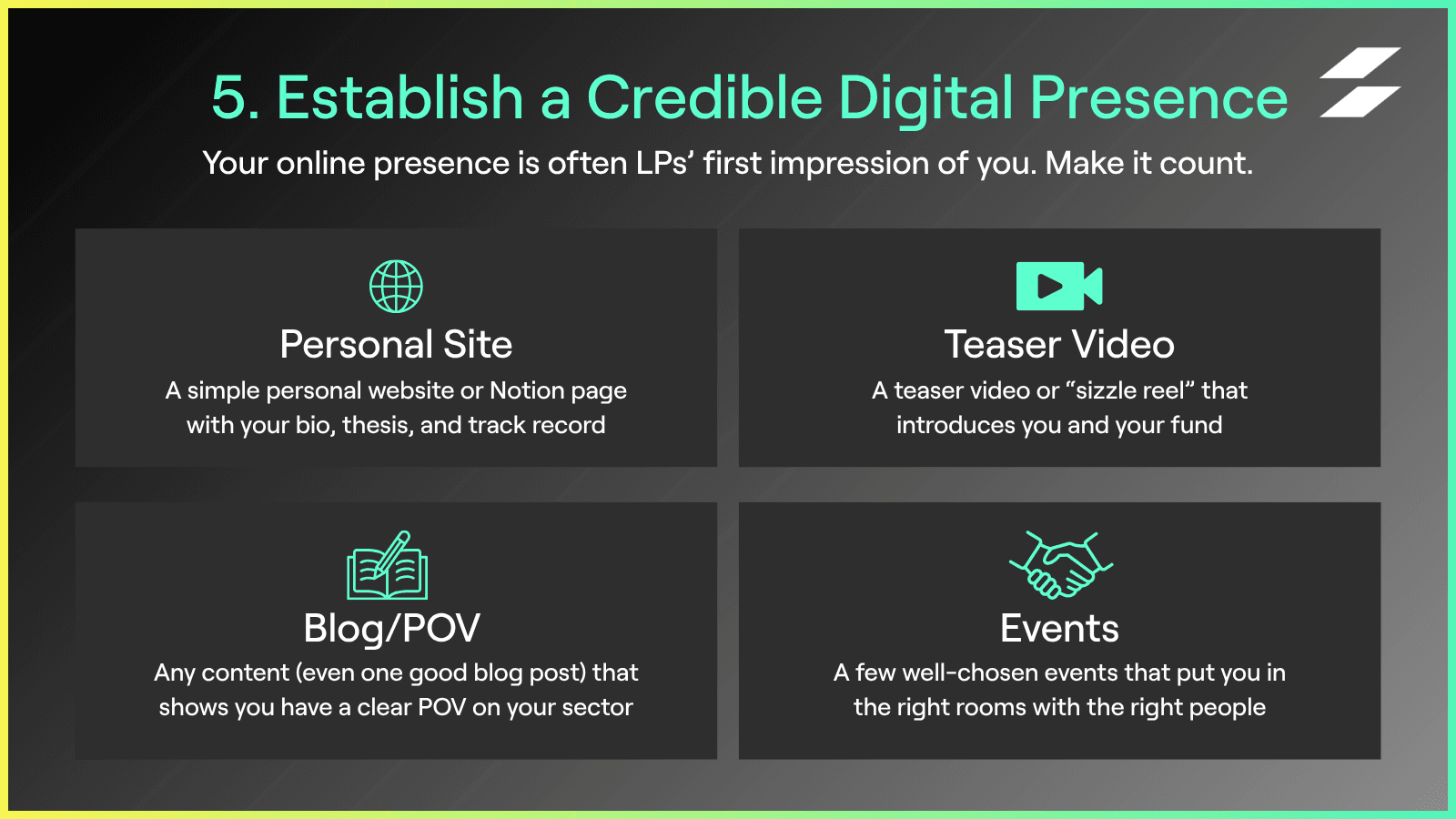

5. Establish a Credible Digital Presence

LPs are just as likely to Google you as they are to read your deck. Having a clean, professional online presence can help establish credibility before you even meet in person.

That’s not to say you have to become a prolific content creator in order to build trust with LPs. What matters is that your website, LinkedIn, and overall digital presence are professional and cohesive. These platforms should clearly communicate your thesis and reflect your credibility as an investor.

In addition to your online presence, participating in in-person events and speaking engagements can meaningfully accelerate fundraising. Whether it’s a panel at an industry conference or a GP-only dinner, these moments help expand your network, deepen relationships, and give LPs a clearer sense of who you are. They also create content touchpoints, such as photos, quotes, or recaps that you can share online or use to re-engage lukewarm leads.

What helps:

A simple personal website or Notion page with your bio, thesis, and track record

A teaser video or “sizzle reel” that introduces you and your fund

Any content (even one good blog post) that shows you have a clear POV on your sector

A few well-chosen events that put you in the right rooms with the right people

A well-structured online presence focused on clarity, not volume, can reinforce your credibility without requiring constant self-promotion or a huge following. Focus on being findable and compelling when someone looks you up. Brandon Alster, Founder and Managing Partner of Sling Ventures, has built a digital presence that checks all these boxes. His website and LinkedIn profile clearly outline his thesis, portfolio, and background, while the short testimonial video on his site makes his story and value proposition instantly relatable. It’s a simple, high-impact approach that helps potential LPs understand who he is and why they should connect.

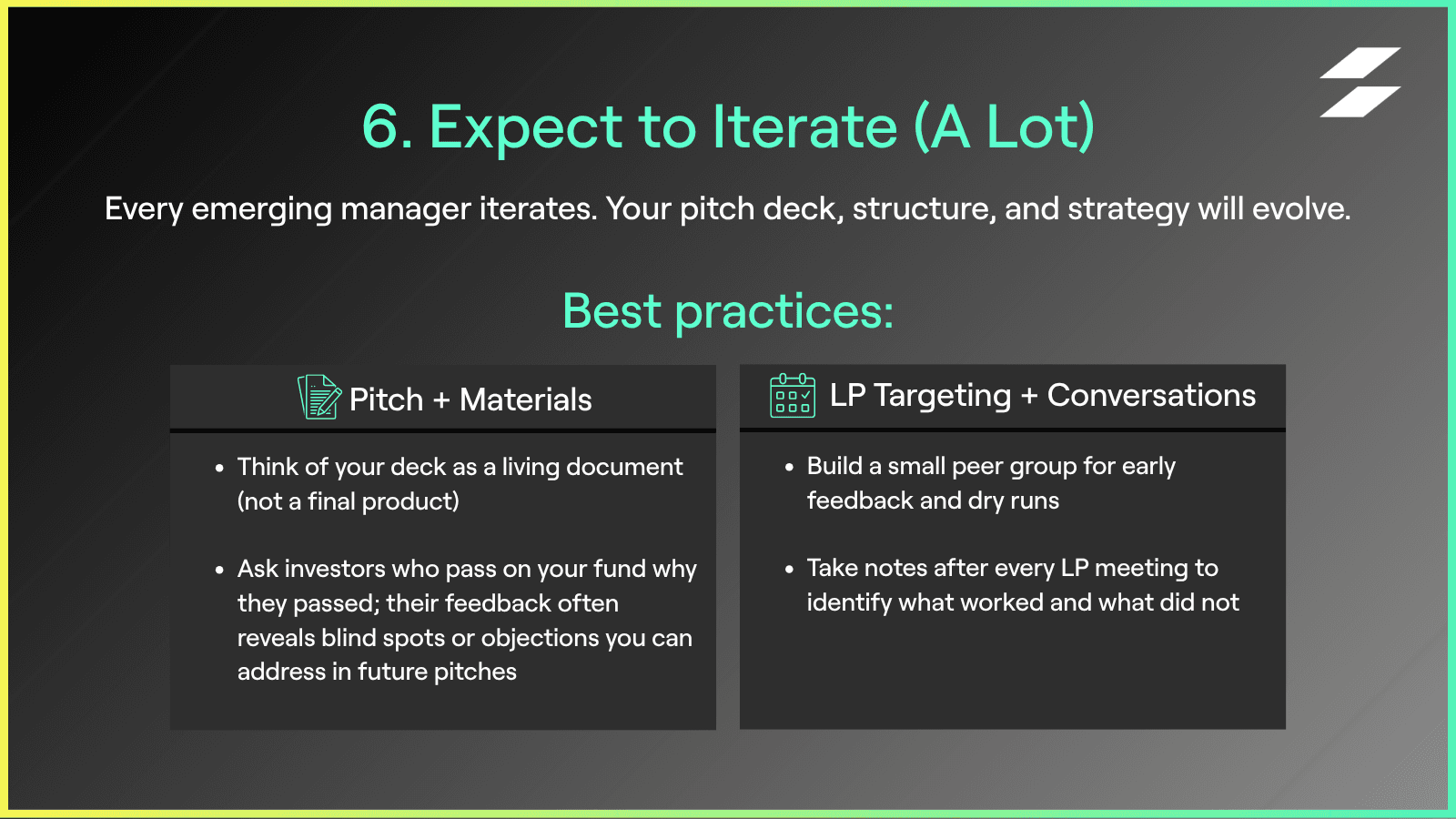

6. Expect to Iterate (A Lot)

Many first-time managers are surprised by how often they need to rework their pitch. It’s normal for even seasoned GPs to go through 20–50 iterations of a pitch before finding the right framing.

Getting feedback, refining your slides, and learning what resonates is part of the process. You should expect to revise your deck, adapt your script, and evolve your positioning over time.

Best practices:

Build a small peer group for early feedback and dry runs

Take notes after every LP meeting to identify what worked and what did not

Think of your deck as a living document (not a final product)

Ask investors who pass on your fund why they passed; their feedback often reveals blind spots or objections you can address in future pitches

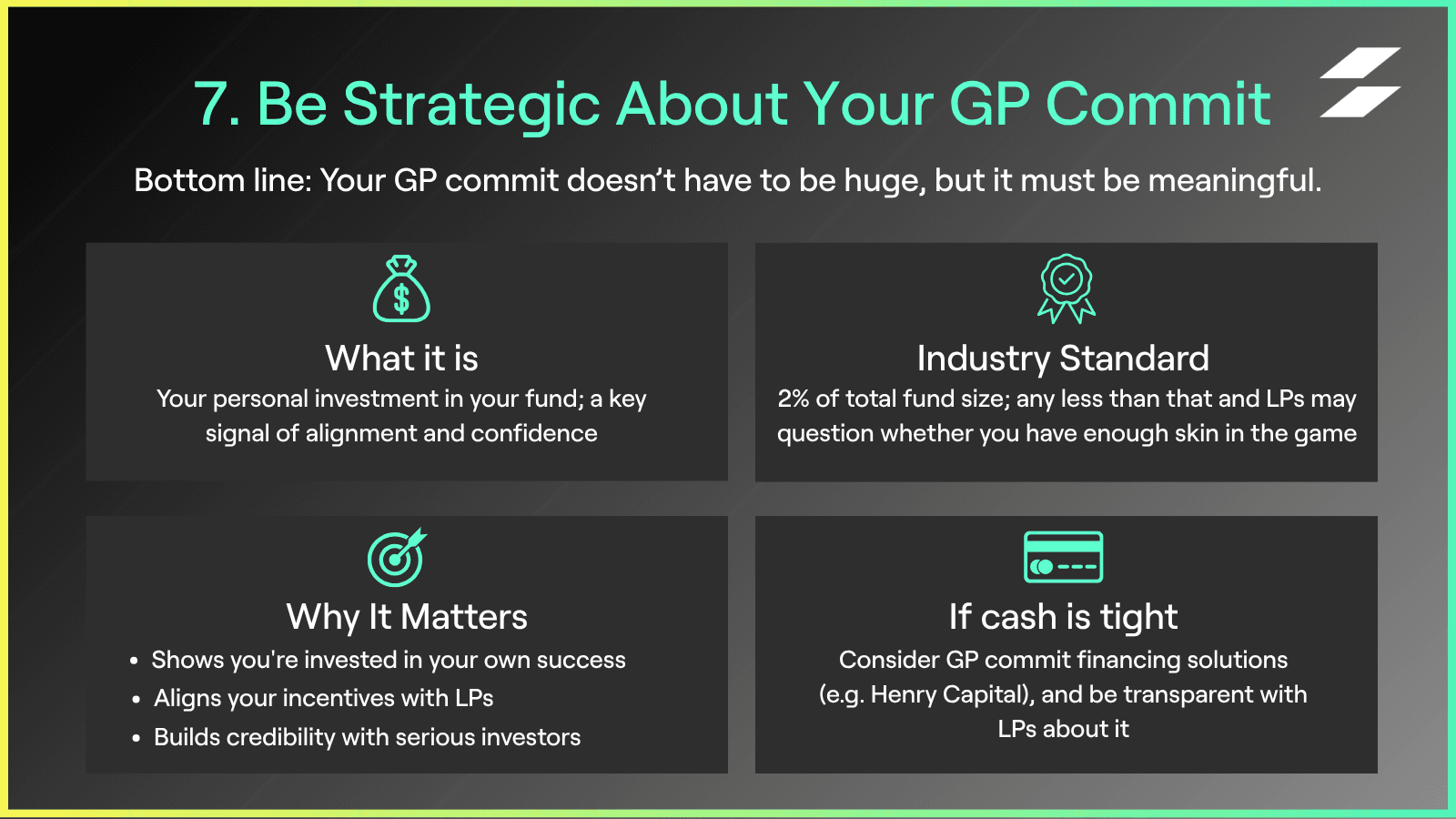

7. Be Strategic About Your GP Commit

As the GP, you need to decide how you’ll approach your commitment, which is a topic that often raises questions for first-time fund managers. The GP commitment is the amount of capital you, as the fund manager, invest into your own fund. Industry standard is typically 2% of total fund size, though some LPs expect more and others are more flexible. Either way, you should be prepared to talk about your approach.

You do not necessarily need to contribute a huge dollar amount, but you do need to demonstrate your investment in your own success and that your interests are fully aligned with your investors. Anything lower than the 2% industry standard could signal misalignment to potential investors.

If capital is a constraint, there are solutions that can front or finance GP commitments, like Henry Capital. Just be transparent with LPs and clear about your rationale.

Closing Thoughts

There is no single path to success as an emerging manager. But the fund managers who succeed, especially in today’s fundraising climate, tend to have one thing in common: they are intentional about how they tell their story, position themselves, and build trust over time.

Use this checklist as a guide, not a formula. The goal is not to check every box. Rather, it is to find the narrative that’s authentic to you and compelling to LPs.

If you want to hear directly from LPs what they look for in an emerging manager pitch, check out our Sydecar Session webinar, "Standing Out as an Emerging Manager: The Pitch":